In Legerity’s recent webinar, we asked an audience of 200 insurance specialists how prepared firms are within their IFRS17 projects.

The effective date of IFRS17 is 1st January 2023 meaning from this point insurance companies will be required to present their financials under IFRS17. The standard demands that one year of comparatives are also shown which means that the transition date cannot be later than one year before the insurers first reported financials in 2023 but can be earlier.

Legerity’s recent IFRS17 webinar covered the data and system challenges of transition, and how a best-practice, cloud-based, IFRS17 architecture can greatly assist your firm to deliver transition seamlessly and with minimal disruption.

During the webinar, we polled the audience on what stage they are in planning for transition. In this article we look at the considerations firms should be making regarding transition.

Not Started

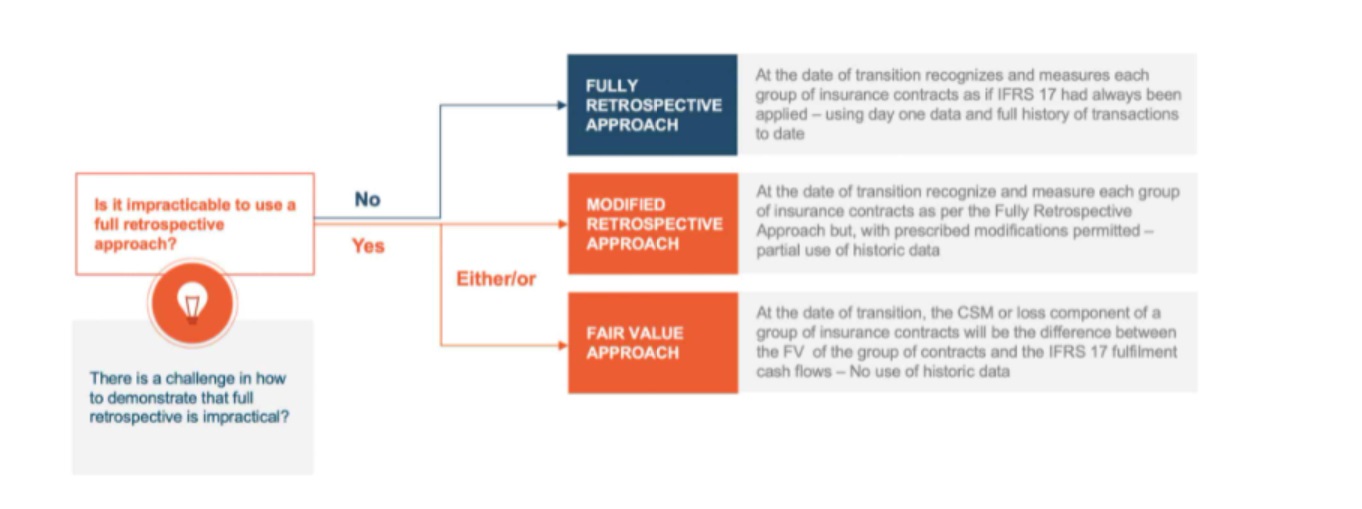

Selecting a Transition Approach

Some firms may have not started thinking about IFRS17 transition yet. Transition is often viewed as one of the more challenging aspects of IFRS17. With a direct impact on the balance sheet and future profits for insurance companies, the choice of which transition approach to use is material.

The basic approach for transition is to prepare your results as if you’ve always done IFRS17. You must look back in time and ultimately produce a view of your financials, on transition, that presumes you had always done IFRS17, but you can approach this in a few different ways.

The table below shows the options available to transition the historical financial information into IFRS17:

To take either the Modified Retrospective Approach or the Fair Value Approach, you need to be able to demonstrate that the Fully Retrospective Approach would be impractical for your firm. You will be relying on your accounting team, and their relationship with the auditors, to have either of those second approaches approved. Fair value is maybe operationally easier, but the calculation of fair value is far from simple.

Early Stage

The Challenges of Transition

The 69% of the audience who were in the early stages of transition will be starting to think about the following challenges:

Data

- The Granularity of data – Going back in time and finding the right granularity of data is going to be tricky. That also includes things like grouping, selection of measurement models and which cashflows are going to be included. The definitions that you need to apply under IFRS17 may not be ones that would have applied in the past.

- Data Availability – Some companies may not have systemised some of their older contracts and supporting data.

- Models – Have you got both the actuals’ data and modelling data that go back in time? In some cases, you will need to investigate those models with a historic lens and forecast from historic points, ignoring what has happened since.

- Hindsight will be key to building up the historic numbers and assumptions will need to be supportable and justified to auditors.

Impact on Results and Understanding

The assumptions you make are going to have a massive effect on the results and how you understand them:

- The recognition of profits on transition and going forward

- Which contacts are onerous

- Reinsurance arrangements on transition and impact on profitability

The effect of IFRS17 on figures will mostly likely inform the tax authorities going forward, but it is not clear exactly what that effect will be

Assessment

So your firm is ready for the transition date, you will need to promptly decide the:

- Transition methods

- Measurement model for all contracts

Not all insurance companies are going to get transition right from day one, so you will have to expect some back and forth on the transition approach. In a way, you will need to build that into your IFRS17 project, and how you manage the transition process.

Processing

Even once your transition process is designed and data prepared you need to consider:

- Time to process data – even if you have aggregated large cohorts in modified retrospective, there can still be huge volumes of data

- You may need to run the transition process more than once

- Cost of processing and storage of these high data volumes